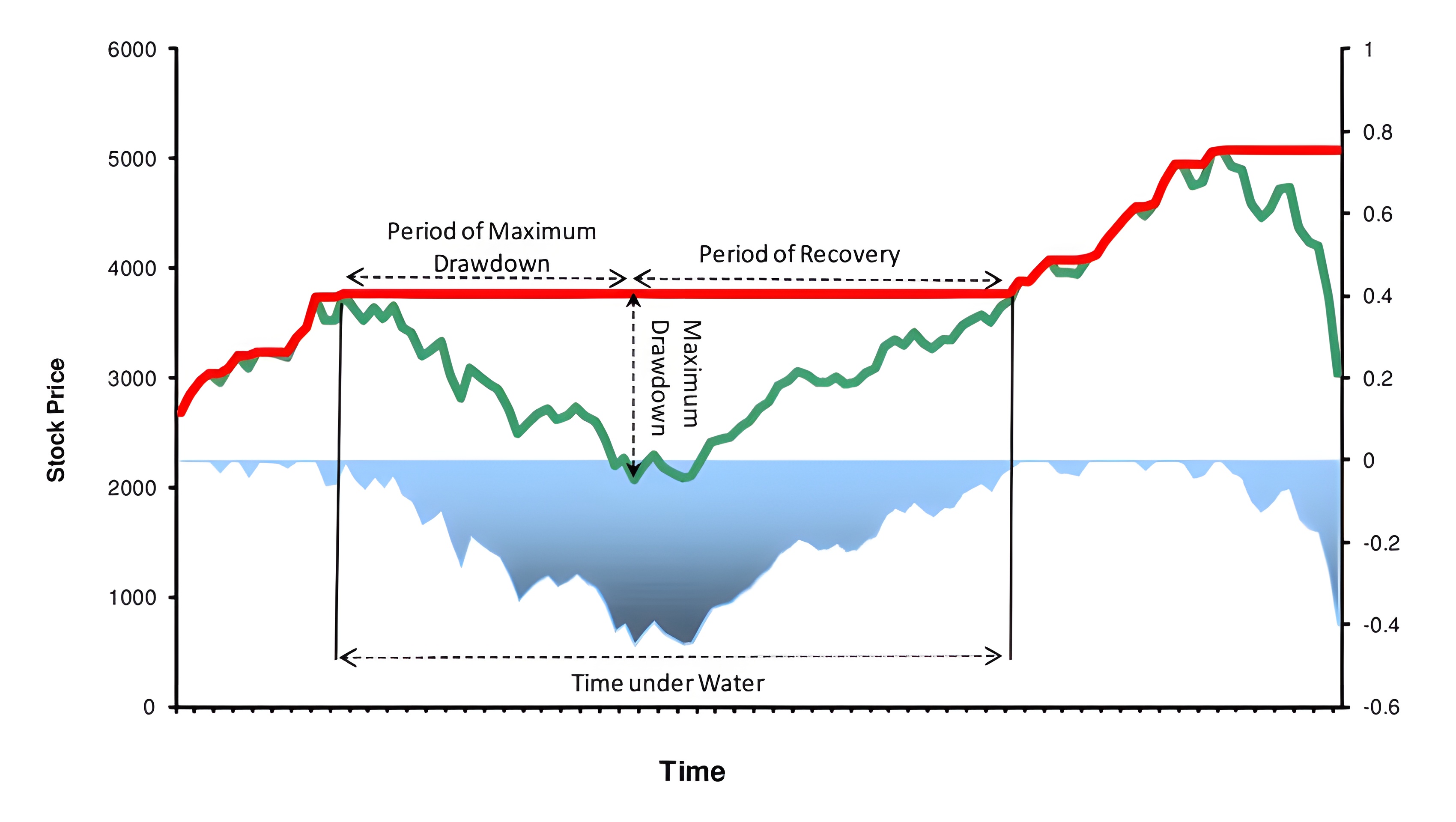

Maximum Drawdown Threshold Indicator

Long-Term Entry-Exit Signal Series

The Maximum Drawdown Threshold belongs to a group of risk indicators, meant to be analyzed on both daily and weekly timeframes.

It quantifies uninterrupted price weakness across multiple timeframes, delivering a concise and layered view of market stress. This indicator is designed to identify periods of extreme undervaluation driven by panic, making it a powerful tool for spotting long-term entry opportunities.

Mostly used on: MQL5, QuantConnect

The Maximum Drawdown Threshold Indicator identifies when an asset has declined significantly from its recent peak, flagging potential capitulation zones. When the drawdown exceeds historically significant thresholds, the indicator signals that the market may be pricing in an unsustainably pessimistic scenario — a classic condition for long-term accumulation.